Data Product is a Crowded Landscape! How Crowded? Take a Look

Zoom back to 2017-18 with me… and think about the idea of using Snowflake, Amplitude or Databricks. At the time, it felt like these companies were alone, operating in a giant ocean of possibility. Fast forward to today, and Snowflake is worth tens of billions, Amplitude just direct listed at a 5+ billion valuation and Databricks, well, that is going to be huge when it hits. That “big ocean” of opportunity still exists, to a degree, but the sea is much more crowded than ever before.

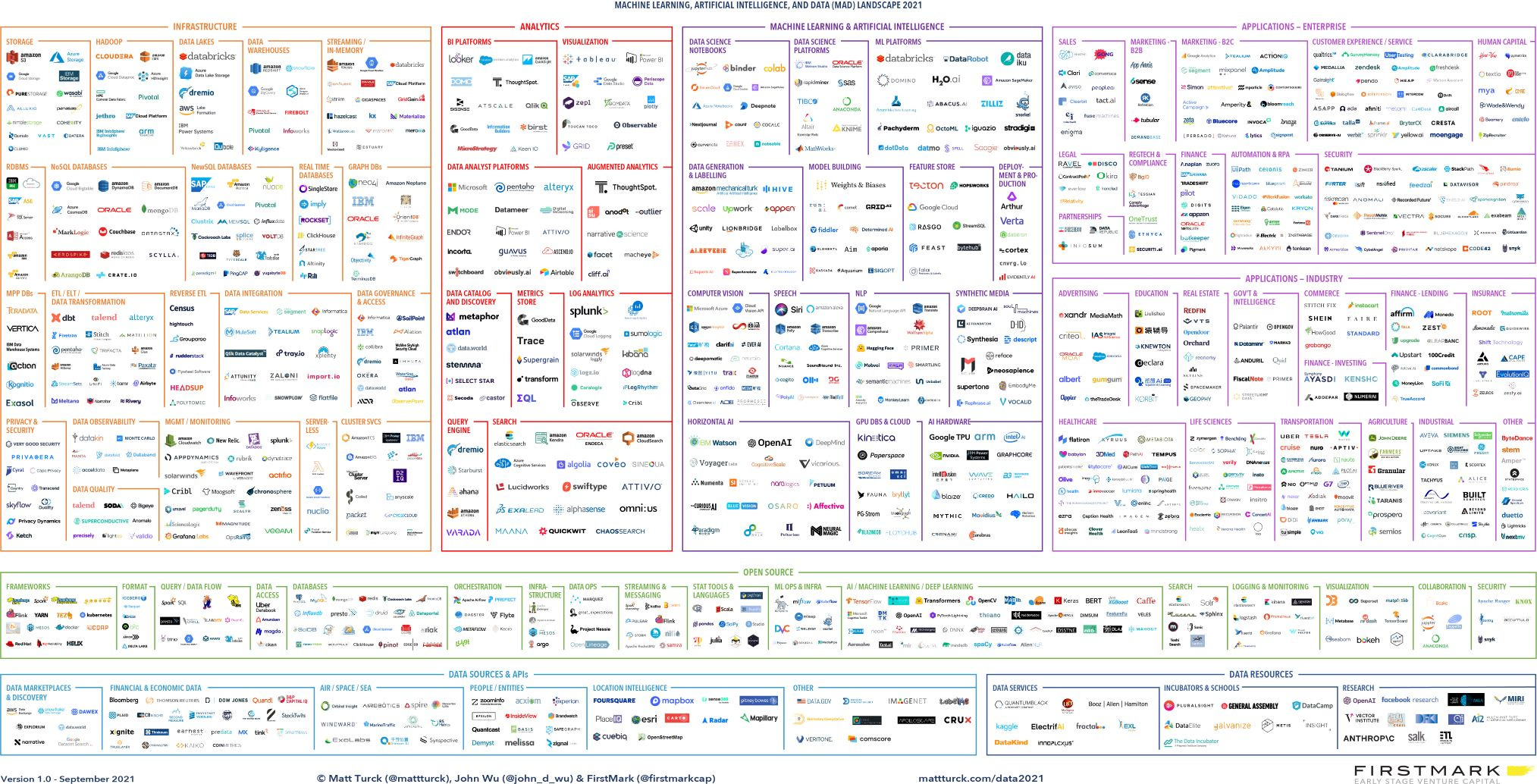

It wasn’t until yesterday that I had a good way to quantify how crowded things have become. I came across an incredible post by Matt Turck, a VC at FirstMark, that illustrates just how wild things are. He expertly broke down all the players (early stage to mature) in different data product areas across the industry in a beautifully laid out approach below:

First all of all, take a moment for your eyes and brain to recover from zooming in and then becoming quickly overwhelmed. Second, take a moment to think about just how incredible it is that an entire space like this has essentially come from nothing in under a decade. Third, I think it is important to think about what this means for those of us who work with and depend on data assets for our company.

Given a full day to digest the post, the diagram and the content within it, I’ve come away with some observations that I think are relevant for those of us working in data product.

The build vs. buy conversation scales have tipped, probably for good, in the direction of buy. Unless a product provides a true competitive advantage for your company and/or literally is intellectual property, it makes very little sense to build your own products and manage them over time. Why? It isn’t just how many options are available. It is that the options available have to compete with each other, making certain areas of data product more commodity-like. While I don’t think we’ll ever fully get to a commodity, competition in the market is good for companies! We should, and will, buy more external products.

A data product manager cannot possibly keep track of an entire market. They need to be focused in a particular domain. The diagram above paints a picture of an absolutely enormous market, with vertical and horizontal components that no single person can possibly “own” or keep up to date with. The data product manager role, all the way up to the CTO role, requires thinking carefully about how to approach this vast domain of options. As I wrote in a previous post, if you expect a data product manager to operate too broadly (e.g. be responsible for ML and experimentation), there’s little chance you’ll be successful.

The role of an product focused engineer continues to evolve. As external options like those above multiply to an incredible degree, I know some engineers feel a threat to the products they’ve built internally. I disagree with that perspective. The tilting of the build vs. buy market actually just shifts the type of work and expertise required. In nearly every company there is a deep sigh that comes out when talking about how much work “integration” takes. But as the dependency on external products increases, integration goes from being a pain to being center stage. The ability to quickly integrate and make best use of external products is an art, and it will likely be paid like one go forward.

The pricing dynamics are going to be fascinating to watch. As I mentioned above, companies in these spaces need to compete with each other. Competition tends to drive down prices (assuming we aren’t going to end up with weird price collusion behind the scenes). This is *good* for everyone. But from what I’ve seen so far, pricing in these areas is the Wild West. I’ve seen some truly wild approaches to charging customers for use, particularly from companies that were early on in their areas. As competition increases, I hope to see more consistency in how pricing and value capture takes place. I imagine that at some point, data product offerings will be commoditized enough that the pricing approach will actually be an important differentiator.

I don’t think there’s enough room in the market for this many data products. I might be very wrong here (and I’ll be happy to own that if it is true), but I don’t see a way in which major consolidation does not take place across these spaces. I believe each of the companies and products listed has enormous value, that’s not the issue. The issue is that customers and enterprises are going to be so confused about what to do when there are this many options. Stitching together a stack consisting of ten different data contracts is going to be a non-starter for many companies who don’t want more complexity. What does that mean? I’m guessing the behemoths in the space (in particular Snowflake and Databricks) are going to go on an acquisition spree in the coming years. It also probably means there are behemoths in waiting, some of which are in this diagram. We just don’t see them that way quite yet.

I truly love working in data product. Its transformational, complex and exciting. Given how much has changed in the last 4 years, imagine what conversations we’ll be having in this space in 2025. I can’t wait. Have a great week!

If you enjoyed this, I’d love to have you subscribe and share below.

I was just talking about #1 internally and have started to evaluate “Product-Led Growth CRMs” along this spectrum (once a co like Calixa rolls out a Snowflake connector, buy feels like a no-brainer).

#4 is exciting in a Jeff Bezosian your-margin-is-my-opportunity kind of way, and I look forward to doing a little arbitrage in niche markets with a couple of side projects.

Re: #5 -

I think the prolific SaaSification of the marketing domain (just look at the first Martech map vs the last!) is informative here. Analytics is finally getting the tooling to break out of the bounds of the BI suite and the wave will similarly stretch TAM — Snowflake as a platform alone will be Salesforce-esque in its gravitational pull for new development over the next decade (imho).

I think we’re going to see the cottage industry of agencies and specialists grow to accommodate companies as they navigate the plethora of options. In turn, additional abstraction layers will keep cropping up, necessitating even more products to keep pace.